University of Petrosani,

Universității no. 20, code 3332006, Petroșani, Hunedoara, Romania, *o2fnbrg@yahoo.com

ABSTRACT

Mining investments in Europe are facing environmental issues, especially those regarding landscape ecology. In this situation, Geoecology, through its multidisciplinary structure, can include specialized elements in the management process, as part of the holistic (exhaustive) evaluation. The paper presents the situation regarding the geoecological audit or the Eco-audit as an element of the evaluation and examination process that involves verification through tests and analyzes performed in order to determine if the legal requirements of the environment can be fulfilled. This element simulates the process and involves at least three stages (pre-audit, effective audit, post audit), being an important management tool.

The manuscript is addressed to specialists involved in mining process with a view to develop the geoecological perspective for this sector and to present some necessary information’s for management, as a good practice.

Keywords: geoecological, environment, audit, accounting, extraction

INTRODUCING

Environment is an expression, a manifestation of the quality of geographical system as dimension of its load with life resources. Intensive and uncontrolled industrial exploitation of natural resources has caused environmental degradation (geographic area affected by humans) and has led to an ecological crisis. The solution identified by the UN was adopting a new concept called Sustainable Development. Although initially wanted to preserve quality of Surrounding Environment further the concept of sustainable development expanded to Quality of Life in its complexity, both economically and socially, remaining so until now. But a sustainable society have as fundamental principle to achieve for its population the quality of life based on growth and sustainable development within its natural system (spatial unit that population is experiencing, in which people live and interact with their environment). Thus, in evaluating the quality of life is a clear distinction between Sustainable Development, which is qualitative change of the system, made in order to maintain the dynamic balance with the environment, and Sustainable Growth which is the quantitative increase of the system loaded with life resources. Quality of life is formed by all the elements related to physical, cultural, economic, social, political, people health conditions, the nature and scope of activities, the characteristics of relations and social processes involving people, goods and services people access, adopted consumption patterns, lifestyles, circumstances evaluation and activities results, subjective states of satisfaction or dissatisfaction, happiness, frustration, etc.

Starting from the definition of quality of life emerges how to measure it, by reference to: state, represented by the standard life of individuals at a time, which is the subject of evaluation, and value, represented by a set of evaluation criteria which consider the state of life. The two elements can be evaluated both individually and combined; individual’s life within society can be considered as activities undertaken by it on, the basis of own initiatives and living conditions of individual. Living conditions are made up by resources of life and frame (matrix) of life.

The resources of life, for any individual, are those reserves or sources of means which he found in his living (surrounding) environment likely to be used at a time to create his own life; can be economic, natural, social, cultural and personal (physical, intellectual, physical, etc.).

The frame of life can be divided, in turn, to individual frame, represented by its living environment (habitat) which influences perceptive, biophysical and psychological the individual and the group frame represented by the social environment used by individual interacting the rest of people within society. In case of a population, given the much greater spatial extent (geographical), to which it refers, living conditions are affected both directly by the two components and synergic by the action of other disturbing factors from society. The main environmental impacts of the industry include issues such waste disposal or water and air pollution. In addition, industry produces greenhouse gases (CO2) and hundreds of millions of tons of solid waste annually, including fly ash, flue or sludge that contains various toxins and heavy metals. But industry it is the only one that can allow economic added benefit relying on natural resources, even there is a battle between society and companies. In the case of mining companies, it is known that they seek to maximize their profit whatever the results, ignoring the environmental effects while authorities try to maximize taxes, revenues and rehabilitation responsibilities. In these circumstances there is a possibility that long-term profitability of mining projects to be affected due increased responsibility for environmental effects of mining activities. Increasing responsibilities involves environmental costs quantified based on assessment and evidenced by accounting values. Costs may be supported by the population/ society (decreasing quality of life, destruction of habitats and ecosystems, loss of biodiversity, changing landscapes etc.), by the mining operators as pollutants, when in the business plan are economic instruments necessary for environmental rehabilitation or both. Criteria for rehabilitation can be very different and therefore appear as either radical current, proposing total elimination of the effects, or different soft trends that suggest establishing an acceptable level of pollution/ contamination of environment. Regarding the pollution/ contamination justification (acceptance), in most of the cases consists by economic logic (benefits reasons).

INDUSTRIAL LANDSCAPE AND POLLUTION

The Industrial Landscape is assimilated to productive activities and brings together those natural or urban areas that conserve essential components (heritage) of the production process, for industrial activities; most time is seen as a “counter-landscape” in relation to natural one. But Industrial Landscape results from practice, decisions and productive activities, being at the same time a part of Cultural Landscape through multiple applications of technical knowledge and social memory that includes. The industrial landscape is what gives value (aesthetic, historical, technical, etc.) to human production activity and not vice versa (Preite, 2009, 2010). [3]

Defined as an open system, industrial landscape has its own structure, containing natural, functional, social, technical and economic elements. The industrial landscape groups one or more industrial units, one or more industrial areas showing a high degree of complexity and diversity. Inside its composition, in addition to the visible material part, are associated aspects related to the memory of the place, social memory, publications, media, techniques, machinery and/or equipment and others representative elements. [3]

OECD Council (1974) defined pollution as “the introduction by man into the environment, directly or indirectly, of substances or energy which causes harmful consequences likely to endanger human health, to harm living resources and ecosystems, bringing touches to approvals or prevent other legitimate uses of the environment”. For industrial units, this definition limits the concept to changes/transformations introduced by man, understanding by substances and energy not only solid, liquid or gaseous materials but the heat, noise, vibration and any other form of radiation which, once introduced in the environment, changes the balance of its constituents or damage living organisms and/or material goods.

To decide how to intervene, the consequences of pollution can be assessed on different levels:

˗ Level I, Bio-ecological stage – related to affected factors (targeted),

˗ Level II, Geoecological stage – related to affected landscapes (holistic),

˗ Level III, Biosphere stage – related to climate change (global).

Usually, first level (I) is about surrounding environment factors while second level (II) is addressed to geographic environment. Most of the productive units can be framed in the second level, from Geoecological/Landscapes Ecology point of view using holistic approach of Geosystems within Geographical Environment where it develops. The task of physical investigation, observation, measurement, evaluation and relating in a holistic way of industrial landscapes inside geographical areas, taking into account the influences arising from functional inabilities and/or abilities generated by the natural and technical actions within geographical environment belongs to Geoecology – the engineering field concerned about geographical systems developments knowledge through a transdisciplinary approach.[3]

GEOECOLOGICAL AUDIT

a. General approach

The connection between geography and ecology, generated by the human society, reached large zones of intersection by defining the two concepts of “Ecosystem” and “Geosystem” (Bertrand, 1978, cited by Pătru-Stupariu, 2012 and Iliaş, 2019). The difference between these two concepts is that the Geosystem (Sochava, 1963, cited by Pătru-Stupariu, 2012 and Iliaş, 2019), as an object of physical geography, has a spatial character while the Ecosystem has a functional one (Mac, 1990 cited by Iliaş and Offenberg, 2019). Also has a smaller number of structural and relational connections (after Preobrajenski, Rougerie and Beroutchachvili, cited by Drăguţ, 2000 and Iliaș, 2019), focused on individuals and/or populations. Geoecology enables the analysis of dynamic combinations for natural and anthropic (technical) factors occurring within a territory where are industrial activities (including natural resources extraction). Geoecological knowledge of geographical systems (Geosystems) evolution is achieved by monitoring (systemic and natural-economical), that includes tracking changes of natural systems and their transformation from natural-technical reasons, including the financial costs involved. On the other hand, Geoecological factors are highly variable and may be useful or not for a company which leads Geoecological audit to detect flows and trends of the geographic systems within enlargement, composition, structure and operation, being different from the simple inventory, which is a specific activity for measuring the time required to quantify the presence, abundance and distribution of ecological factors by surrounding environment where a company operate. [1]

b. Principles

ISO 19011:2011 provides guidance on auditing management systems, including the principles of auditing. It replaces ISO 14012:1996, Guidelines for environmental audit, whose purpose was standardization in the field of environmental auditing and related environmental investigations. In principle, there is a process of assessment and review, involving analysis, tests and confirmations whose aim is to check how a company, as whole or certain structure components, satisfy local or national legal requirements in a specific field, thus complementing the overall management. Therefore, Environmental Audit (E-A), or Eco-Audit, could be a management tool used to establish performance measures in environmental protection. [4]

As concept, it appeared in the 70’s in order to assessment environmental performance of activities in the chemical and oil industry, but in time expanded because the following factors:

- Environmental accidents frequency increasing,

- Considerable tightening of environmental legislative and regulatory constraints,

- Intensifying protest of civil society and NGO on environmental protection issues,

- Applying the "Polluter-Pays Principle[1]" for environmental remediation.

Environmental audit differs from other techniques of assessing relationship between the environment and technical-economical work (production) because Environmental Impact Assessment (EIA) refers to the identification, planning, normalization, measuring and communicating environmental effects potentially associated with an investment project (including mining), while Environmental Audit (Eco-Audit) is an activity focused on the systematic analysis of real environmental performance that characterizes all the activities of a company involved in that project. The environmental audit is intended to be an exhaustive examination of management systems and facilities, without understanding through this activity a full and effective way of solving all environmental problems generated by an economic operator. EA goal remains to determine compliance status or level of compliance of an operator for satisfying declared, self-imposed and imposed (legal) requirements through a systematic collection and assessment of objective evidence. [4]

Usually, environmental audit involves, but are not confined to, carrying out activities, such as: Pre-audit, Audit (verification) and Post audit.

1. Pre-audit stage, shall include: selection of analyzed sectors, choice the team, the plan, the purpose and the schedule, resource allocation, documents preparation and obtaining information.

2. Audit stage, shall include: proper understanding of system and procedures, detailed analysis for establishing the legality and regularity of all proposed operations and compliance with environmental protection principles, sound environmental management (SWOT), recommendations schedule and responsibilities.

3. Post audit stage, shall include: reporting implementation of solutions, recommendations, responsibilities and monitoring, in order to have a second layer of assurance on the legality and regularity; that can be carried out by an independent audit.

Practices led to outline some trends, such as:

- Extending the applicability due to increased demand for green products and services, including new economic areas, mandatory consultation of communities, gain social movements for environment, including environmental conservation as performance parameter in relation to the insurers;

- More severe control on the EA report, standardization of techniques, procedures and reports;

- Increasing business efficiency by integrating EA within environmental management system and accepting this practice as an expression of the will of managers or Good Practice.

VALUE OF LANDSCAPES

The problem of the landscape’s assessment developed a whole literature and is undoubtedly the most discussed are about areas administration and planning. Issues to the economic value of landscape appears early in the 70’s, with reference to the value of land associated with the cost of housing located to a certain range near a green space (forest, park, public garden). But the concept has been developed since the 90’s starting to the assessment of agricultural and forestry landscapes when outlined a new science – Economy of landscape. In this respect the emergence of numerical modeling of the landscape to the price of a geographical area was associated with the “open landscape”, respectively the landscape visible from a point. [5] Marangon & Tempesta (2008) proposed a model for assessing the costs for valuation, recovery and preservation of landscapes starting from “desideratum that the landscape is a place to live and leisure for communities, but also offers specific services related to the preservation of biodiversity and ecosystems; these actions are of interest to both present and future generations”, that is why the value of landscape could be estimated as a cost-benefit assessment (CBA).

The benefits are grouping values generated by:

- areas that can be arranged, taking in account the landscaping,

- existing landscape, through planning, tourism activities, recreation, and

- indirect or non-use benefits (architectural, historical, cultural monuments etc.).

The costs can be related mostly to:

- conservation of landscape,

- maintenance (roads, buildings, green areas, gardens, woods etc.).

According to the proposed methodology, the direct costs can be related to an average hourly wage for each category of inventory activity. At the same time, economic value is based on the marginal utility of a good, while the cultural value of an object or activity is based on aesthetic, spiritual or religious, social, historical, symbolic and identity value (Throsby, 2001).

Starting from the notion of cultural value, Throsby (2001) conceptualizes cultural capital as "an asset that stores cultural value in addition to its economic value", and applies the theory of sustainable development to cultural capital, called the principle of intergenerational equity ("the justice of the intertemporal distribution”).[6] In this regard, if the current reserve of cultural capital is allowed to diminish (e.g. by lack of investments in industry, environment, agriculture) future generations will be deprived of benefits produced by this reserve, because their interests will no longer be reflected on the current market (Sache, 2009). Sache retains the following evaluation methods, used by Bănacu [8] for the built cultural heritage:

˗ comparing the sale price approach, which involves identifying a property with characteristics as similar as those of the assessed heritage (called comparable property). The criteria for selecting the comparable property refer to location, architectural style, size, cultural and historical characteristics. The valuation of the patrimony will be made in comparison with the sale price of the comparable property, adjustments being made if the assessed patrimony requires restoration / rehabilitation works or when it is the subject of contracts with restrictive provisions;

˗ income approach, used in the case of the built heritage that is capable of generating commercial or rent revenues, its use in this respect being the most effective alternative. The evaluation will take into account, in addition to the estimated income to be obtained, the possible restoration / rehabilitation works that may be necessary for the use of the good, the period of time required to obtain the necessary authorizations (if it is necessary to authorize the commercial use of the respective heritage element), as well as the additional expenses with the preservation of the heritage that arise as a result of its introduction / reintroduction into the economic / commercial circuit;

˗ by cost approach, based on the assumption that the built cultural heritage has intrinsic value (due to the appearance, certain characteristics or status of symbol). Its value will be determined taking into account the cost of producing a replica of the heritage element or, if this is not possible, the cost of making a modern building with a similar purpose. The application of this method will take into account the cost of preserving the built heritage, as well as the reduced possibilities of adapting it to the specific needs of the occupant. If the company opts for a strict control of the phenomenon of environmental pollution, the standard quality and the level of degradation had to be specified. Because the criteria underlying their adoption are very different, divergent currents of opinion have emerged, starting from the total elimination of the environmental effects to the abandonment of the affected perimeters in the form that exists when the activity ceased.

For a unitary approach, the followers of the conventional economy propose to establish an "optimal level of contamination", considering that any contamination process must be associated with both costs and benefits. [4] This approach considers that it is very important to know the ability to recover and / or assimilate the changes that have occurred for natural-technical reasons, for each individual case, because when this capacity is exceeded, the effects of landscape transformation appear and the pollution process can start to has an economic meaning, requiring the determination of the "optimal level of environmental pollution". [7]

In this regard, Ruijgrok (cited by Iorgulescu, 2011) considers that the economic value of cultural heritage can be defined by the level of "welfare" that it generates for society. In establishing the economic value of the cultural heritage, it must be taken into account that it can present a value of use (it generates benefits through its use) and / or a value of non-use. The value of non-use comes in three forms:

˗ the option value (for individuals who have not visited the respective cultural heritage site but wish to do so in the future),

˗ the value of existence (for individuals who have not visited the site and do not intend to do so in the future but who perceive the existence of the site as a positive fact),

˗ the value of inheritance (the value of the knowledge transmitted by the cultural heritage for the benefit of future generations).

He thus observes that the economic evaluation of the cultural heritage allows the use of the cost-benefit analysis when estimating the investment benefits in the conservation of the heritage and of the losses caused by the destruction of the heritage elements, which can lead to the influence of the economic decisions and cause its destruction. [7]

The Romanian school contributes to the development of this concept, Negrei (2004) proposing a model of determination having as objective function the maximization of social welfare, thus:

[W] = [P] + [E] (1),

Where, [W] represents social welfare, respectively the value associated with the environment [E] and of productive works, goods and services [P] (production). [4]

Negrei (cited by Preda, 2005) analyze the relation (1) and observe that the ideal situation is a production P1 that does not eliminate pollutants and generates environmental effects E1 without making any expense for environmental protection (null). Thus, he proposed two new relations:

[P1] – [P] = [C] (2),

and

[E1] – [E] = [D] (3),

Where [C] represents the cost of control or the value of the means used to combat technical pollution and [D] represents the environmental damage caused by technical pollution. [4]

[Wo] = {[P1] – [P]} + {[E1] – [E]} = [C] + [D] (4),

Where [Wo] represents the optimal welfare obtained by minimizing the total costs (means used and damages).[4]

Despite all the attempts of the economic theory to base as accurately as possible an optimal pollution, there are no generally accepted general models. The optimization tendency cannot have a real and completely support if it does not surprise the processes of transforming some "free goods" considered for a long time unlimited (e.g. water, air, wind, sun) into economic goods. This process of reconsidering free goods as economic goods becomes more and more important as their limited character is highlighted. Even if free goods do not diminish quantitatively as they are used in production processes, the quality (purity, accessibility, allocation and others) can undergo transformations in the sense of diminution. So, we rarely find clean air and pure water. In these conditions, environmental externalities appear when the private costs differ significantly from the social costs, deforming the mechanism of optimal allocation of resources. Social costs may include direct or indirect effects incurred by a community through hospitalization, medications, medical leave, relocation and stress due to economic activities that aim to maximize profits and minimize technical costs. All these costs should be found in the costs of technical transformations [ET]. In the same time, a company must support not only costs of technical transformations [ET] but also costs of landscape changes and/or transformations by natural reasons [EN]. This means that the environmental issues must be analyzed holistic by considering all complementary and/or synergistic influences added/subtracted to the technical ones, using geoecological damage [DG]. [1]

From the Geoecological perspective the new relation is

[Wo] = {[P1] – [P]} + {[E1] – [ET±EN]} = [C] + [DG] (5),

Where

[E1] – [ET±EN] = [DG] (6).

In conclusion, the authors propose that the identification of the optimum point of the social welfare of the landscape implies the evaluation of:

- Control costs, as investments and the means necessary to control environmental factors,

- Geoecological damage, such as the loss/deterioration and/or transformation of the Geosystem respectively landscape’s aptitudes/inaptitude’s to produce.

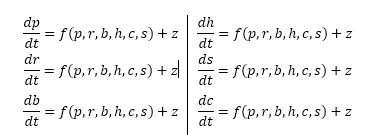

Without being limiting, the economic evaluation is made based on a geoecological analyzing and lists drawn up after prior identification of the landscape structure (factors) and changes in the landscape structure (impact), including lists (sets) of elements with aptitudes/ineptitudes induced in the Geographical environment formed by: pedolithosphere, relief, biosphere, hydrography, society, climate and the surrounding environment; they can be adjusted according to the type of system analyzed. This geoecological analysis can be formalized by descriptive relationships of the components of the Geosystem from geographical environment where: Pedolithosphere– p, Relief– r, Biosphere– b, Hydrography– h, Society– s and Climate– c. [1]

The system of equations of this “prbhcs” model is:

A simplified conceptualization can also be obtained by using matrix relations:

Where x is a vector of the state variables that describes the Geosystem under study, f(x) is the matrix that defines the interactions between the state variables and z is a vector of the auxiliary variables. The interaction between the components of the Geosystem can be defined by the parameters type aij, the complete set of parameters can be written as an interaction matrix (I), of type "nxn" which can be added to the equation. The economic evaluation of the landscapes value should highlight the dynamics of cost generated by the alternation between:

˗ uniformization respectively structural diversification and/or different ways of development (fast - slow, discrete - continuous) generated by the disruptive processes,

˗ the regeneration potential respectively the risk of natural components elimination from geographical environment by background changes (natural) or natural and cultural (anthropic) transformations, as follows:

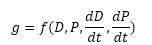

Where g is a property of the Geographical environment (e.g. degree of artificiality/ transformation), D is a set of dynamic vectors, P is a set of passive vectors and dD/dt and dP/dt are the rates of change over time.

ENVIRONMENTAL ACOUNTING

Starting from the System of National Accounts (SNA), which is a measurement framework that has been evolving since the 1950’s to embody the pre-eminent approach to the measurement of economic activity, economic wealth and the general structure of the economy, during the 60-70’s it broke down the idea of environmental accounting. The framework can be used to analyze and evaluate various aspects of the economy (e.g. its structure, specific parts, development over time) yet for some specific data needs, such as analysis of the interaction between the environment and the economy, the best solution is to draw up separate satellite accounts. It appeared as a necessity to apply the accounting concepts, structures, rules and principles to environmental assessment by integrate environmental information (often measured in physical terms) with economic ones (often measured in monetary terms) in a single framework. Satellite accounts allow the analytical capacity of national accounting to be expanded for selected areas of social concern, such as pressures on the environment stemming from human activity, in a flexible manner, without overburdening or disrupting the central system; should be made available to the public regularly and in comprehensible form. [10] The integration of all these data concerning the economy and the environment requires an interdisciplinary approach to bring together, in a single measurement system, information from pedolithosphere, relief, biosphere, hydrography, society and climate; regarding but not limited to people, water, minerals, energy, timber, soil, land and landscapes, ecosystems, pollution and waste, production, consumption and/or accumulation.

In 1987, the Brundtland Commission Report entitled Our Common Future (World Commission on Environment and Development, 1987) made clear the links between economic and social development and environmental capacity. Later in 1992, Agenda 21 adopted at the United Nations Conference on Environment and Development, held in Rio de Janeiro, called for the establishment of a “Programme to develop national systems of integrated environmental and economic accounting in all countries”. In response, the United Nations Statistical Division published the Handbook of National Accounting: Integrated Environmental and Economic Accounting (United Nations, 1993) commonly referred to as the SEEA. This handbook was issued as an “interim” version of work in progress, since the discussion of relevant concepts and methods had not been concluded. [9] The system of integrated environmental economic accounts (SEEA), developed collectively by the United Nations, the European Commission, the International Monetary Fund, the Organization for Economic Cooperation and Development and the World Bank, is a satellite system of the SNA. In order to ensure uniform conditions for the implementation of SEEA Framework on 6 July 2011 the European parliament and of the council was adopted the Regulation (EU) no 691/2011 on European environmental economic accounts. [10] The power of the SEEA Framework comes from its capacity to present information in both physical and monetary terms coherently.

In practice, environmental-economic accounting includes the compilation of physical supply and use tables, functional accounts (such as environmental protection expenditure accounts) and asset accounts for natural resources. The Central Framework covers measurement in three main areas: (a) the physical flows of materials and energy within the economy and between the economy and the environment; (b) the stocks of environmental assets and changes in these stocks; and (c) economic activity and transactions related to the environment.

Measurement in these areas is translated into a series of accounts and tables: (I) supply and use tables in physical and monetary terms showing flows of natural inputs, products and residuals; (II) asset accounts for individual environmental assets in physical and monetary terms showing the stock of environmental assets at the beginning and the end of each accounting period and the changes in the stock; (III) a sequence of economic accounts highlighting depletion-adjusted economic aggregates; and (IV) functional accounts recording transactions and other information about economic activities undertaken for environmental purposes.

The analysis of these data can also be extended by linking the tables and accounts to relevant employment, demographic and social information. [9]

CONCLUSIONS

Environmental management arose due to concerns of promoting ecological principles. As a result, many of the environmental management initiatives lack the holistic integrated vision and often are confuse. Thus, under this name only found general environmental concerns, many statistics data and very few real ideas about policies and strategies to be followed. But, the environmental management of a company must allow leadership to ensure that:

- Whole activity complies with all legal and regulatory provisions;

- Internal operations, organization, structure and procedures are clearly defined;

- The environmental risks of the company are known and are under control;

- The company has provided funds and environmental services.

Within management pyramid, environmental activities belong to:

- Strategic management – mission, corporate objectives, business ethics and social responsibility;

- Operational management – energy consumption, raw materials and clean technologies;

- Financial management – environmental costs;

- Human resource management – environmental education.

Therefore, it should be more clearly defined role, duties and involvement of each area of management (strategic, operational, financial personnel and environmental) in the environmental protection activities.[4] In a well-organized company environmental management is supplemented by other functions of enterprise management, so there must be interconnections between them, such as:

- Planning – setting goals, policy orientation, procedures, program’s budget;

- Organization – establishing organizational structure, defining roles and responsibilities, establishing qualification and training of staff;

- Guiding and directing – coordination, motivation, prioritizing, developing performance standards, disturbances and changes in administration;

- Communication – developing and implementing effective communication channels of business within departments and with external groups including convenient regulatory organs;

- Control and provision – measuring results, knowledge performance, taking corrective measures.

Strategically, ecological obligation is placed in relation with social responsibility, which can be graphically represented as a pyramid with four dimensions: economic, ethic, legal and discretionary. Most often, at the bottom of this pyramid is placed economic responsibility (respectively to be profitable and manage costs), over which are overlaps legal responsibilities (compliance with laws and regulations). In this respect, in the second stage we find ecological responsibility while in the third and fourth are ethics (correct information) and discretionary (contribution to improving life conditions). [4] Every stage generates costs easier or more difficult to quantify. Different cost categories are usually supplementary to the basic investment, being dedicated to obtain low-impact by research and development of products/services, adaptation and modernization of work technology, training and development of staff and inform the community and the interested/affected individuals. Environmental costs are reflected in final prices depending on social and environmental responsibility of the mining operator, the price sensitivity of the beneficiaries and finally the market position and applied strategy. Any strategy has mainly four modes of manifestation: (1) Reactive, if there is no ecological involvement unless expressly requested, (2) Defensive, when avoiding taking responsibility by inhibiting factors that could attract it, (3) Adaptive, measures are taken when required by law and/or community and (4) Proactive, when action is taken on its own initiative and continuously.

Whatever the strategy, from economic point of view, as a good practice, environmental management should lead to further cost recovery by creating competitive advantage in the market, as trying to avoid translating the costs to final consumers. Geoecological audit highlights the multiple links between systems that shows most mines can affect the landscapes only within low geographical scales. If the effects are reduced as extension and with natural potential of evolution is not justify avoiding or stopping the investments.

REFERENCES

[1] Offenberg I., Iliaş N., Radu S.M., Geoecology and geotechnologies, Ed. AGIR, Bucharest, Romania, 2019.

[2] Offenberg I., Environmental management and geoecology for the mining sector, Ed. Impressum, Chişinău, Republic of Moldova, 2018.

[3] Iliaş N., Radu M.S., Offenberg I., Geoecology of life quality - loading with living resources of the Geographical Environment, Chișinău, Republic of Moldova, 2019.

[4] Preda G., Puiu A., Capitalization of natural resources, International University Press, Bucharest, Romania, 2005.

[5] Pătru-Stupariu, I., Structural and functional modeling of landscapes, Bucharest University, Romania, 2012.

[6] Iorgulescu, F., Alexandru F., Creţan, G.C., Kagitci M., Iacob M., Theoretical and applied economics - Volume XVIII, Bucharest, Romania, 2011.

[7] Offenberg I., Iliaş N., Radu S.M., Serafinceanu A., Teşeleanu G., Offenberg A., The industrial landscape - An economical option, International Conference - Economic growth under the conditions of globalization: welfare and social inclusion/Ed. XIV, National Institute of Economic Research (INCE), Chişinău, Republic of Moldova, 2019.

[8] Bănacu, C.S., Practical guide to real estate appraisal, Ed. Economical Tribune, Bucharest, Romania, 2007.

[9] United Nations, System of Environmental Economic Accounting 2012 - Central Framework, New York, 2014, https://ec.europa.eu/eurostat/documents,

[10] Regulation (EU) no 691/2011 of the European parliament and of the council of 6 July 2011 on European environmental economic accounts, https://eur-lex.europa.eu/legal-content.

[1] The Polluter-Pays Principle was adopted by the OECD Council in 1972 in its Recommendation on Guiding Principles Concerning International Economic Aspects of Environmental Policies as an economic principle for allocating the costs of pollution control, http://legalinstruments.oecd.org.